Regular readers will know I take a keen interest in the regulatory role of the Appointed Actuary. See my previous posts here, here and, most recently, here.

This week APRA released a consultation package with proposals on how the role should be changed to make the role fit better into the regulatory and management framework of life insurers. APRA is asking for written submissions in response by 15 December 2017. So you have a bit of time to read the detail.

At first glance, though, the package is similar to the high level proposals made last year, with some changes in detail and consideration of how the changes would fit into the existing prudential standards framework. As well as proposing draft standards and guidance notes, the big addition is the proposal to add private health insurance Appointed Actuaries to the framework, now that APRA regulates them also.

APRA has retained the overarching statement of the purpose of the Appointed Actuary, with some changes to words suggested by submissions:

The purpose of the Appointed Actuary role is to ensure that the board and senior management have unfettered access to expert and impartial actuarial advice and review. The role is intended to assist with the sound and prudent management of an insurer and ensure that the insurer gives appropriate consideration to the protection of policyholder interests.

The Appointed Actuary must have the necessary authority, seniority and support to contribute to the debate of strategic issues at a senior management level and provide advice that is considered seriously by the board. The Appointed Actuary plays a key role in, and provides effective challenge to, the activities and decisions that may materially affect the insurer’s financial condition, as well as policyholder interests.

Having this overarching statement will be very helpful in helping stakeholders understand the role of the Appointed Actuary, emphasising as it does financial condition and policyholder interests.

APRA has emphasised in the proposed draft guidance note that this does not preclude the Appointed Actuary being an external appointment (as is common in general and health insurance, particularly for smaller companies). And while many submissions suggested that the Appointed Actuary should be a direct report to the CEO of the organisation, APRA prefers to leave organisation structure up to companies, rather requiring “necessary authority, seniority and support”.

APRA has also proposed a very short list of items that are reserved for the Appointed Actuary to provide advice on:

- The Financial Condition Report

- The Actuarial Valuation Report, which is a widened Insurance Liability Valuation report (not required, but encouraged, for health insurers). This report is not required to be provided to the Board, but must be sent to APRA.

Each of these reports has a relatively short list of requirements that must be considered for inclusion.

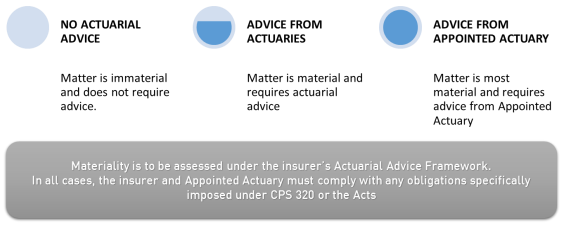

And then each company must create an actuarial advice framework. As part of the framework, the company must consider, for a number of specific items, whether actuarial advice is required, and if so, whether that advice must come from the Appointed Actuary. For each type of insurer (each has its own list), this is broadly those items that are currently required to be the subject of actuarial advice from the Appointed Actuary:

- For all insurers – the various key methodology and assumptions requirements of policy liability and capital calculations (but each type of insurer has specific words and requirements here)

- For life insurers – pricing, investment strategy and reinsurance strategy

- For health insurers – a long list of business changes such as pricing, business plans, strategic plans and product development

My favourite section in the whole consultation package was this one from the draft Prudential Practice Guide:

APRA is aware of instances in which the Appointed Actuary of an insurer is temporarily absent, and this has caused logistical challenges for insurers [my emphasis]. In some cases the absence is planned, such as annual leave, and in other cases the actuary may have been temporarily incapacitated [my emphasis]. To alleviate these challenges, while respecting the requirements in the Acts that a single specified individual occupies the statutory Appointed Actuary role, a framework for temporary appointments of Appointed Actuaries can be created and documented as part of the actuarial advice framework.

An insurer may nominate an individual or individuals under this framework who can temporarily replace the Appointed Actuary if necessary. Only one individual may be the Appointed Actuary at any particular point in time. Any individual occupying the Appointed Actuary role is required to be appropriately qualified and satisfy the fit and proper requirements under CPS 520. An insurer may find it useful to complete a fit and proper assessment of the nominated individual(s) ahead of time, so that they can be expeditiously appointed to the Appointed Actuary role if necessary.

Right now, the Appointed Actuary regime, particularly for life insurers (with its requirement for actuarial advice before a company makes material pricing changes and before a company makes any changes to reinsurance), is the biggest source of key person risk to a life insurer. If an Appointed Actuary is sick, then there are a number of aspects of a life insurer’s business that must stop until a new Appointed Actuary can be appointed, as delegation is not allowed by the legislation. It is good to see that this consultation package proposes to fix this in two ways – by allowing for actuarial advice from other actuaries in the business as part of an actuarial advice framework, and making it simpler to nominate a replacement in the case of planned or unplanned leave.

Overall, my first impressions are that the package is a good pragmatic response to the current inconsistent and task based regulatory regime for Appointed Actuaries in the various types of insurers. I first wrote about those inconsistencies (particularly for Life Insurance) early in 2012, So while I’m sure imperfections remain, I hope the next steps don’t take too long, so that we can move reasonably quickly towards a more coherent framework.

Creating an appropriate environment for an Appointed Actuary to have the right level of influence in an insurer can’t be done with a regulatory environment alone – the culture of the company, the capabilities of the incumbent and the reputation of actuaries in the company will all be important. That said, these proposals seem to be moving in the right direction – taking away the compulsion of the compliance parts of the role that don’t require the strategic oversight of an AA. So I am supportive on the whole. I look forward to the next steps.

For this post, I am re-emphasising my disclaimer. While I am currently an Appointed Actuary of a life insurer, and the Appointed Actuary of a general insurer reports to me, this post consists of my own personal views, and does not necessarily reflect the views of either of those insurers, or my employers – past, present or future.

___________________________________________________________________________________________________________

I was amused to see the proposals reported on in The Australian under the headline APRA seeks to grant actuaries greater powers:

The prudential regulator has proposed giving actuaries unprecedented access to insurance company boards, auditors and senior executives as it looks to put companies on the hook if they ignore the advice of their boffins…

…The rules would see actuaries writing reports on the financial condition of insurers, which would be submitted to APRA. Insurers would be beholden to provide the actuaries with huge amounts of access to company committees, internal auditors, external auditors, senior management and others if requested by the actuary.

The actuary would advise companies on the value of their liabilities, the adequacy of their risk charges, the level of capital held and the calculation of stress-tested models.

Those aspects, picked up by the Australian, don’t add any powers to the access and reporting already required from all Appointed Actuaries. As APRA says in its preamble, though, the intent is to increase the strategic contribution from Appointed Actuaries, particularly in life insurance, by removing or reducing some of the compliance reporting that really should be part of a well-regulated risk management framework without requiring actuarial oversight.